1031 Exchanges: A Complete Guide for North Texas Real Estate Investors

1031 Exchanges: A Complete Guide for North Texas Real Estate Investors

There's a line you hear constantly from experienced real estate investors: "Never pay taxes on a property you sell." They're referring to Section 1031 of the Internal Revenue Code — one of the most powerful wealth-building tools available to any property owner in the United States, and one of the most misunderstood.

A 1031 exchange isn't a loophole. It's a deliberate provision in the tax code that has existed since 1921, designed to encourage the reinvestment of capital into productive real estate. When you use it correctly, you can sell an investment property that has appreciated significantly, roll all of the proceeds into a new property, and pay zero tax on the gain at the time of sale. The tax isn't forgiven — it's deferred, carried forward in your basis — but for investors who plan their exits thoughtfully, the deferral can last a lifetime, and in the right circumstances, permanently disappear at death.

In the Dallas-Fort Worth market, where investment property values have compounded aggressively over the past decade, 1031 exchanges are an increasingly central part of how sophisticated investors manage their portfolios. A rental home bought in Prosper in 2014 for $280,000 might be worth $550,000 today. A small commercial building purchased in Frisco a decade ago has likely done even better. Selling those assets without a 1031 exchange triggers capital gains tax plus depreciation recapture — a combined federal bill that can easily reach 25 to 30 percent of the gain, before Texas income tax (which doesn't exist, an advantage Texas investors already have).

This post covers how 1031 exchanges work from the ground up, with enough depth to let you have an informed conversation with your CPA, your attorney, and your qualified intermediary — the team you need around you before any exchange begins.

The Core Concept: Deferral, Not Elimination

The most important thing to understand about a 1031 exchange is what it actually does to your taxes. It doesn't make the gain go away. It defers the gain into the replacement property by reducing your tax basis.

Here's how that works in simple terms: you sell a property for $800,000 that you originally paid $400,000 for. Normally, you'd pay capital gains tax on the $400,000 gain. In a 1031 exchange, you instead acquire a replacement property. Your basis in the new property is not its purchase price — it's the purchase price minus the deferred gain. If you pay $900,000 for the replacement property, your new tax basis is approximately $500,000, not $900,000.

When you eventually sell the replacement property, that deferred gain comes due — unless you do another exchange, in which case it defers again. Investors who continue exchanging into successively larger or more suitable properties defer the tax indefinitely. The strategy has a name: "swap till you drop" — because when you die holding property, your heirs receive it with a stepped-up basis equal to its fair market value at the date of death, permanently eliminating the accumulated deferred gain. Generations of accumulated tax deferral can vanish at death.

The scale of that benefit, compounded across decades of exchanges, is why Section 1031 is one of the most significant provisions in the tax code for real estate investors.

What Qualifies: The Basic Requirements

Not every property sale qualifies for 1031 treatment. The IRS has four fundamental requirements that must be met before any exchange can proceed.

The property must be real estate. Since the Tax Cuts and Jobs Act of 2017, Section 1031 applies exclusively to real property. You cannot exchange vehicles, equipment, collectibles, or business personal property under Section 1031 any longer. Real property is broadly defined — it includes land, improvements to land (buildings, structures), and certain property integrated into or affixed to real estate.

The property must be held for investment or productive use in a trade or business. This requirement eliminates two common categories: your primary residence and property held primarily for sale. A fix-and-flip property — purchased specifically to resell after renovation — does not qualify because the intent is sale, not investment or business use. A rental property, commercial building, raw land held for investment, or property used in your trade or business qualifies. Vacation homes are a gray area addressed by its own IRS guidance (Revenue Procedure 2008-16), which requires at least two years of ownership and documented rental use meeting specific thresholds.

Both properties must be in the United States. U.S. real property is not like-kind to foreign property, full stop. If you own an investment property in Mexico and want to exchange it, Section 1031 is not available to defer that gain into domestic property or vice versa.

The exchange must be of "like-kind" property. This is where most first-time investors overestimate the restriction. "Like-kind" in the context of real estate is remarkably broad. It refers to the nature or character of the property, not its type, grade, or quality. A single-family rental home is like-kind to a commercial office building. Raw land is like-kind to an apartment complex. A duplex is like-kind to a warehouse. As long as both properties are U.S. real estate held for investment or business use, they are almost certainly like-kind to each other. You can use a 1031 to trade out of the landlord business entirely — selling residential rentals in exchange for a net-lease commercial property where a national tenant handles everything — as long as the property qualifies under the other requirements.

The Tax Exposure You're Deferring

To understand what's at stake in a 1031 exchange, you need to understand the taxes you're deferring. There are potentially three separate layers.

Long-term capital gains tax applies to the appreciation in the property's value above your adjusted cost basis. For most investors, the federal rate is 15 percent. For taxpayers with higher incomes, it's 20 percent. Texas has no state income tax, which gives DFW investors a meaningful advantage over investors in California (up to 13.3% state rate), New York, or other high-tax states.

Depreciation recapture is often the tax that surprises investors most. When you hold investment real estate, you're generally entitled to depreciate the improvements (not the land) over 27.5 years for residential rental property and 39 years for commercial property. That annual depreciation deduction reduces your taxable income every year you hold the property. When you sell, the IRS recaptures all of the depreciation you've claimed — or were entitled to claim — at a federal rate of 25 percent. This is called unrecaptured Section 1250 gain. For a property held many years with substantial depreciation deductions taken, this can be a significant number.

Net Investment Income Tax (NIIT) adds an additional 3.8 percent federal tax on investment income (including capital gains) for taxpayers whose modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly). This tax is often overlooked in early planning conversations but can substantially increase the effective tax rate on a sale.

Put these together and a Texas investor in the 20% capital gains bracket with significant depreciation recapture could face a combined federal tax rate approaching 28 to 30 percent on their gain — on the gain itself, not the gross sale price. On a property that has appreciated $500,000 with substantial accumulated depreciation, that's a real number. A properly structured 1031 exchange defers all three layers.

The Exchange Structure: How It Actually Works

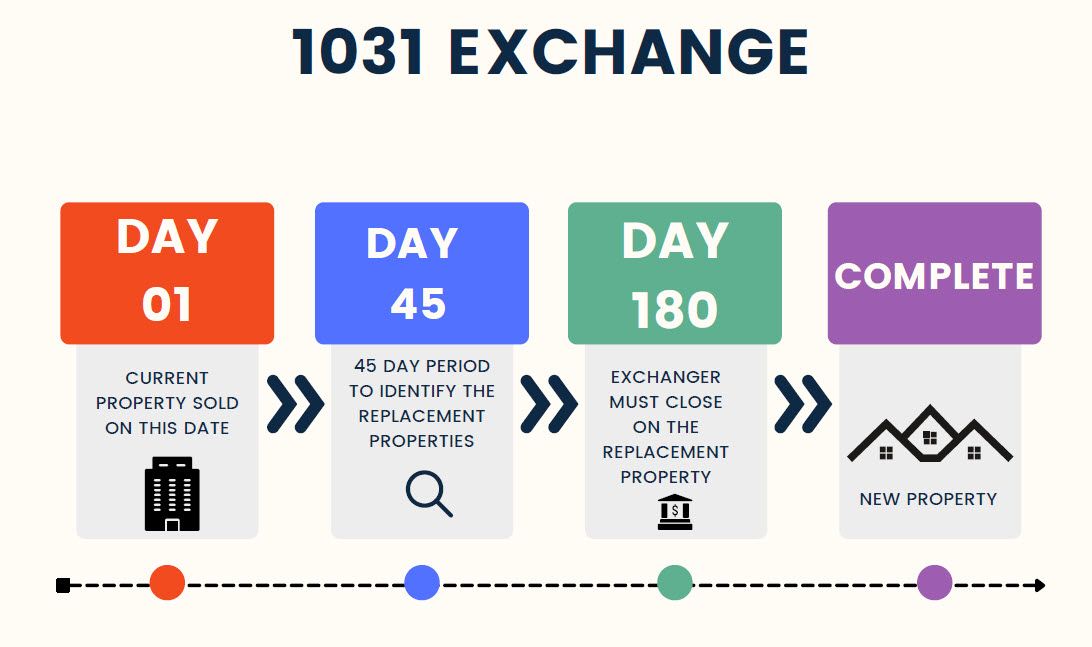

The simplest conceptual version of a 1031 exchange — simultaneously swapping your property directly with another investor — almost never happens in practice. What actually happens in the overwhelming majority of real-world transactions is a deferred exchange, also called a forward exchange.

In a deferred exchange, you sell your property first, and the proceeds are held by a qualified intermediary while you locate and purchase a replacement property. The tax code requires this structure because if you receive the sale proceeds yourself at any point — even briefly — the exchange is disqualified. Your actual or constructive receipt of the funds triggers the taxable gain immediately. This is not a technicality. It's one of the most common ways exchanges fail, and it cannot be fixed after the fact.

The mechanics of a forward exchange work like this:

You list and sell your investment property. Before the closing on the relinquished property, you engage a qualified intermediary (discussed in detail below) and establish the exchange agreement. At closing, the proceeds from your sale do not flow to you — they flow directly to the qualified intermediary, who holds them in a segregated escrow account. From that moment, two clocks start running simultaneously.

You then search for and identify a replacement property within 45 days, and close on it within 180 days. The QI uses the escrowed funds to purchase the replacement property on your behalf. Done correctly, you never have access to the money, the exchange qualifies, and the gain is deferred.

The Two Deadlines: Strict, Non-Negotiable, and Critically Important

The timing rules for a 1031 exchange are the area where most failed exchanges die. They are exactly as rigid as they sound.

The 45-Day Identification Period

From the date you transfer the relinquished property — the closing date on your sale — you have exactly 45 calendar days to identify potential replacement properties in writing. Calendar days means exactly that: weekends and holidays count. If Day 45 falls on a Sunday, you don't get Monday. The identification deadline is midnight of the 45th day.

The identification must be in writing, signed by you, and delivered to the qualified intermediary or another permitted party (not your attorney, real estate agent, or accountant — they are disqualified persons in this context). The identification must describe the replacement property with sufficient specificity: a street address, legal description, or in some cases the name of a Delaware Statutory Trust interest.

There are no extensions for running out of time to find a property. There are no extensions because the market is competitive or your first choice fell through. The only extensions granted are for federally declared disasters under Revenue Procedure 2018-58 — and those apply only to affected taxpayers in designated areas.

The 180-Day Exchange Period

You must close on the replacement property within 180 calendar days of your relinquished property closing — or before your tax return is due for the year of the sale (including extensions), whichever is earlier. That second condition catches investors who close late in a calendar year. If you close on the relinquished property in November, your 180th day might be in May, but your tax return could be due April 15 without an extension. Filing an extension can be important to preserve the full 180-day window when exchanges span into a new tax year.

Like the 45-day deadline, 180 days does not extend for weekends, holidays, or market conditions.

The practical implication is that you should begin searching for replacement properties before you close on the relinquished property, not after. Investors who list a property, go under contract, and only then start thinking about what to exchange into routinely find themselves scrambling. The 45-day window is shorter than it feels when you're actually in it.

The Three Identification Rules

Within the 45-day identification period, you must follow one of three IRS rules governing how many properties you can identify and at what values. You choose which rule to apply, and you can only use one rule per exchange.

The Three Property Rule

You may identify up to three potential replacement properties, regardless of their combined value. This is the most commonly used rule because it's the simplest and provides meaningful flexibility. Identifying three properties gives you backup options if your first choice falls through or negotiations fail. Most residential and small commercial investors use this rule.

One important nuance: identifying three properties doesn't mean you have to close on all three. You just have to close on at least one. Many investors identify their primary target and two backup properties as a risk management measure.

The 200% Rule

You may identify any number of potential replacement properties, as long as their combined fair market value does not exceed 200 percent of the value of the relinquished property. If you sold a property for $1,000,000, you can identify as many properties as you want as long as their total value doesn't exceed $2,000,000. This rule is useful when you want to identify more than three properties — for example, if you're considering multiple smaller properties or assembling a portfolio.

The value used for the 200% calculation is the fair market value at the time of identification, not the contract price. Keep documentation of how you determined fair market value for any properties you identify under this rule.

The 95% Rule

You may identify any number of properties for any aggregate value, as long as you actually close on at least 95 percent of the total fair market value of everything you identified. This rule is almost never used deliberately — it only makes sense if you intend to actually acquire the vast majority of your identified properties. More often, investors fall into this rule accidentally when they've overidentified properties under the 200% rule and the math stops working out. It's a trap, not a strategy.

The Qualified Intermediary: Who They Are and Why They Matter

The qualified intermediary (QI) — also called an exchange accommodator or exchange facilitator — is the legally required third party who holds your exchange funds and executes the exchange on your behalf. You cannot do a deferred exchange without one.

The IRS specifically prohibits certain people from serving as your QI. They call these "disqualified persons" and the category includes your attorney, your accountant, your real estate agent, your employee, or anyone who has provided any of those services to you within the past two years. A family member is also disqualified. The QI must be a truly independent party with no prior agent relationship with you.

The QI holds real money — your entire sale proceeds — often for up to 180 days. There is no federal licensing requirement for QIs, no mandatory bonding or insurance requirement, and no oversight agency that supervises their operations in the way that banks or broker-dealers are supervised. This creates meaningful counterparty risk. Several high-profile QI failures have resulted in investors losing their exchange funds entirely when the QI became insolvent, was defrauded, or committed fraud themselves.

When evaluating a QI, look for:

Fidelity bonds and errors and omissions insurance. These protect you if the QI makes a mistake or commits fraud. Ask for proof of coverage and verify the amounts.

Segregated accounts. Your funds should be held in an account separate from the QI's operating funds and separate from other clients' exchange funds. If a QI commingles exchange funds with their own accounts, you're exposed if the QI faces any financial difficulty.

Track record and institutional backing. A QI that is a subsidiary of a large title insurance company or bank has resources and oversight that a sole-practitioner QI does not. National firms like IPX1031, Asset Preservation, and Old Republic Exchange are commonly used by Texas investors with national footprints and established reputations.

Clarity on interest. The QI earns interest on your escrowed funds during the exchange period. Some QIs keep this interest; others pass it through to you. Clarify this arrangement upfront. On a $1,000,000 exchange held for 120 days, the interest is not trivial.

QI fees. Expect to pay $750 to $2,500 for a standard single-property exchange. More complex exchanges — reverse exchanges, improvement exchanges, multiple properties — cost more. The fee is a small fraction of the tax deferred and is worth paying for a reputable firm.

Boot: The Taxable Exception Inside a 1031 Exchange

"Boot" is the term for any portion of an exchange transaction that is not like-kind — and it's taxable in the year of the exchange, even in an otherwise successful exchange. Boot doesn't invalidate the exchange; it just creates a partial tax event.

Boot comes in two forms.

Cash boot occurs when you receive cash out of the exchange. If you sell a property for $900,000 and only buy a replacement property for $750,000, the $150,000 difference flows back to you as cash — and that's taxable. Similarly, if you take money out of the exchange funds for any purpose before closing on the replacement property, that amount is boot.

Mortgage boot (also called debt relief) occurs when the mortgage on the replacement property is lower than the mortgage on the relinquished property. If your relinquished property had a $300,000 mortgage that was paid off at closing, and your replacement property only has a $200,000 mortgage, the $100,000 reduction in debt obligation is treated as boot. You received economic benefit — relief from debt — that wasn't reinvested into like-kind property. This surprises investors who trade down in debt structure.

The three-part rule for avoiding boot is:

- The replacement property's value must equal or exceed the relinquished property's value

- The replacement property's debt must equal or exceed the relinquished property's debt (or equity reinvested must make up the difference)

- All cash proceeds from the sale must be reinvested

An important and painful detail: boot is taxed in a specific order. The IRS applies the most expensive tax rate first. Depreciation recapture — taxed at 25% federally — is allocated to boot before capital gains rates are applied. So if you have boot and you have accumulated depreciation, expect that boot to be taxed at 25%, not at the 15% or 20% long-term capital gains rate.

Depreciation Recapture in Depth

Because depreciation recapture is one of the most significant and most misunderstood elements of a property sale, it deserves its own discussion.

When you own investment real estate, the IRS assumes the improvements (the building, not the land) are wearing out over time. Residential rental property is depreciated over 27.5 years; commercial property over 39 years. Each year, you can deduct a portion of the building's value as a depreciation expense against your rental income, reducing your taxable income.

That sounds like a benefit — and it is, during the holding period. The problem surfaces at sale.

When you sell, the IRS recaptures all the depreciation deductions you've claimed (or were entitled to claim, whether you claimed them or not) at a federal rate of 25 percent. This is unrecaptured Section 1250 gain. The word "unrecaptured" in this context means depreciation not already taxed at ordinary income rates under Section 1245, which doesn't generally apply to residential real estate improvements.

Here's why this matters: if you've held a rental property for 15 years and taken $150,000 in depreciation deductions, that $150,000 is subject to 25% recapture tax when you sell — $37,500 in federal tax, regardless of whether the capital gains rate on the rest of your gain is 15% or 20%. A 1031 exchange defers that recapture tax along with the capital gains. The depreciation rolls into your basis on the replacement property, and the recapture event is postponed.

The compounding problem: Every time you do a 1031 exchange, your basis in the replacement property is reduced by all the deferred gain — both the appreciation and the accumulated depreciation recapture. After multiple exchanges over decades, an investor's adjusted basis can become very small relative to the current property value. The tax liability carried in that low basis is substantial. The "swap till you drop" strategy addresses this: die holding the property, and the stepped-up basis at death permanently eliminates that entire accumulated liability.

Types of 1031 Exchanges

While the deferred forward exchange is by far the most common structure, there are several other exchange types worth understanding.

Simultaneous Exchange

Both the relinquished and replacement properties close on the same day. In practice this is rarely achievable — coordinating two separate closings for the same investor on the same day, with clean title on both properties, is logistically difficult. When it works, it's simple; when the timing slips, the exchange fails.

Delayed (Forward) Exchange

This is the standard structure described above. Sell first, hold funds with QI, identify within 45 days, close on replacement within 180 days. The overwhelming majority of real-world 1031 exchanges use this structure.

Reverse Exchange

In a reverse exchange, you acquire the replacement property before you sell the relinquished property — the opposite order from a forward exchange. This is more complex and more expensive, but it's the right structure when you find the ideal replacement property before you're ready to sell your current holding.

The IRS provides a safe harbor for reverse exchanges under Revenue Procedure 2000-37. The structure uses an Exchange Accommodation Titleholder (EAT) — a special-purpose entity — to hold either the replacement property (parked until you sell the relinquished) or the relinquished property (parked until you sell it after acquiring the replacement) during the exchange period. The same 45-day identification and 180-day exchange deadlines apply, running from the date the EAT acquires the parked property.

Reverse exchanges are significantly more expensive than forward exchanges — costs typically run $4,000 to $8,000 or more in QI and legal fees — and they require coordination between the QI, the EAT, lenders, and title companies who are all familiar with the structure. Not all lenders will lend into a reverse exchange structure, which can complicate financing the replacement property purchase. If you're considering a reverse exchange, start with an experienced QI who regularly does them, not one who has done a few.

Improvement (Build-to-Suit) Exchange

An improvement exchange allows you to use exchange funds not just to acquire replacement property but also to fund improvements on it. This structure is used when the replacement property needs work to equal the value of the relinquished property, or when you want to build out a property specifically.

Like reverse exchanges, improvement exchanges use an EAT to hold the replacement property while improvements are constructed or funded from exchange proceeds. The improvements must be completed and identified within the 180-day exchange period. The value of the completed improved property (structure plus improvements) is what counts toward the like-kind requirement. Any improvements not complete by the 180th day don't count — only the value of improvements actually completed before the exchange period closes qualifies.

Improvement exchanges are specialized, expensive, and require careful coordination. They're commonly used by investors transitioning into net-lease commercial properties who want to fund tenant improvements or by investors building out a property to a specific use.

The Same Taxpayer Requirement

The taxpayer who sells the relinquished property must be the same taxpayer who acquires the replacement property. This is called the same taxpayer requirement, and it creates complications in situations involving multiple owners, partnerships, and entity structures.

If a property is held in a partnership (or an LLC taxed as a partnership), the partnership is the taxpayer — not the individual partners. The partnership must do the exchange, and all partners participate together. You cannot have one partner who wants to exchange and another who wants cash out — at least not cleanly. The partner who wants cash can take their distribution before or after the exchange, but doing so requires careful structuring to avoid disqualifying the exchange.

Drop and swap is the common solution when partnership owners have divergent goals. Before the sale, the partnership distributes undivided ownership interests in the property to the individual partners (the "drop"). Each partner then holds their fractional interest individually. Some exchange their interest; others sell their interest for cash. The problem is timing: the IRS looks at when the property interest was received and whether it was held for investment purposes. Partners who receive their interest shortly before a sale and immediately exchange it into a 1031 are at risk of having the IRS challenge the holding requirement. Partners who receive their interest, hold it for a meaningful period as an investment, and then exchange are on firmer ground.

Swap and drop reverses the order: do the exchange at the entity level, acquire the replacement property, then distribute interests to the partners who want liquidity. This is often cleaner from a timing standpoint but creates its own complications around the replacement property distribution.

Entity structure questions in 1031 exchanges — LLCs, LPs, tenancy in common interests, related parties — are complex territory that requires a CPA and real estate attorney familiar with 1031 transactions. Do not attempt to solve entity structure challenges without professional guidance.

Delaware Statutory Trusts: The Passive Investor's 1031 Solution

Delaware Statutory Trusts (DSTs) have become one of the most significant developments in the 1031 exchange market over the past decade, and they're increasingly relevant for North Texas investors who want to exit active property management without triggering a large tax event.

A DST is a legal entity formed under Delaware law that holds title to one or more investment properties. Investors purchase fractional "beneficial interests" in the trust — think of it as a fractional ownership stake in a larger property that you couldn't afford or manage yourself. The IRS has ruled that properly structured DST interests qualify as like-kind real property for Section 1031 purposes.

The practical significance: a landlord who has managed rental properties for 30 years and wants to exit active management can sell their property, do a 1031 exchange, and invest the proceeds into a DST holding institutional-grade properties — Class A apartment complexes, national tenant net-lease retail locations, industrial facilities, medical office buildings — without lifting a finger in management. The DST sponsor (a professional real estate firm) handles all property management, leasing, financing, and reporting. The investor receives passive income distributions and depreciation benefits.

Why DSTs solve a specific 1031 problem: Many investors, particularly those late in their exchange cycle or in a competitive market with compressed cap rates, find it difficult to identify suitable replacement properties within the 45-day window. A DST can be identified and closed on quickly — often within days — making it an excellent backup option to include among your identified properties if your primary replacement property falls through. Some investors use a DST as their entire replacement, while others use it to absorb the "leftover" equity that doesn't fit into a conventional property purchase.

The mechanics: The minimum investment in most DSTs starts at around $100,000. Investors can diversify across multiple DSTs — different property types, different geographies, different risk profiles — using a single exchange. This creates diversification that individual property ownership doesn't provide.

The tradeoffs: DSTs are illiquid. You cannot sell your beneficial interest on the open market the way you'd sell a stock. DSTs typically have a hold period of 5 to 10 years before the sponsor sells the underlying property and distributes proceeds. At that point, investors must do another 1031 exchange with their proceeds, pay the taxes, or accept the taxable gain. DSTs also carry the risks of the underlying real estate, the quality of the sponsor's management, and the financing structure used at the trust level (which is typically non-recourse debt that investors cannot control).

One important DST-specific note on depreciation recapture: unlike direct property ownership where cost segregation studies can accelerate depreciation and affect the recapture calculation, DSTs generally don't allow investors to conduct their own cost segregation studies on the trust's properties. The recapture calculation is determined by the sponsor's accounting, not your own tax strategy.

Estate planning: DST interests are easier to divide among heirs than a physical property, which requires unanimous agreement among all heirs to sell or refinance. The stepped-up basis at death applies to DST interests exactly as it does to direct property ownership, making them compatible with the "swap till you drop" estate strategy.

Calculating Your Basis After an Exchange

Understanding how your tax basis changes in a 1031 exchange is essential for future tax planning, including what happens when you eventually sell without exchanging.

In a clean exchange with no boot:

Adjusted basis in the replacement property = Purchase price of the replacement property − Deferred gain

Or equivalently:

Adjusted basis in the replacement property = Adjusted basis in the relinquished property + Any additional cash paid out of pocket

Example: You purchased a rental property in Allen, Texas for $300,000 ten years ago. You've taken $75,000 in depreciation deductions over the years, making your adjusted basis $225,000. The property is now worth $600,000, and you sell it.

Your realized gain: $600,000 − $225,000 = $375,000 (of which $75,000 is depreciation recapture and $300,000 is capital gain appreciation).

You exchange into a replacement property you purchase for $700,000 using your $600,000 in proceeds plus $100,000 of new cash.

Your adjusted basis in the replacement property: $225,000 (carried over from the relinquished property) + $100,000 (additional cash you paid) = $325,000.

The replacement property is worth $700,000, but your basis is $325,000. That $375,000 gap is the deferred gain — it will be taxed when you eventually sell without exchanging, or it disappears permanently if you die holding the property.

Every subsequent exchange compounds this calculation. An investor who has exchanged four times might own a property worth $3,000,000 with an adjusted basis of $150,000. The deferred tax embedded in that position is enormous — and so is the incentive to continue exchanging or to hold through death.

What the IRS Requires at Tax Time: Form 8824

When you complete a 1031 exchange, you must report it on Form 8824, Like-Kind Exchanges, filed with your income tax return for the year of the sale of the relinquished property. This is true even if no gain is recognized — the exchange still requires reporting.

Form 8824 requires the following information:

- Description of the relinquished and replacement properties

- Dates of transfer and acquisition

- Fair market values of both properties

- Your adjusted basis in the relinquished property

- Any liabilities assumed or transferred

- Any boot received

- The deferred gain calculation

The reporting year follows the sale of the relinquished property, not the acquisition of the replacement property. If you sold your relinquished property in November 2025 and closed on the replacement property in February 2026, Form 8824 goes with your 2025 return (the year of the sale).

Keep meticulous records. The IRS can ask for documentation of any exchange transaction, and you need to be able to reconstruct the entire chain — exchange agreement, QI documentation, closing statements, identification notice, and the basis calculation that resulted from the exchange — potentially for decades after the transaction if the deferred gain is still embedded in the property at audit time.

Common Mistakes That Sink Exchanges

Touching the money. If the sale proceeds flow to you at any point — even into your bank account temporarily "while you find a QI" — the exchange is over. Constructive receipt triggers the taxable event. Set up your QI before you close on the relinquished property, not after.

Failing the 45-day deadline. Investors who are confident they'll find a property and don't take the identification deadline seriously discover there are no extensions when they run out of time on Day 44. Start your replacement property search before closing on the relinquished property.

Incorrect identification. The written identification must describe the replacement property with sufficient specificity. "A single-family home in Frisco" is not sufficient identification. A street address or legal description is required. Vague or insufficient identification invalidates the exchange.

Using a disqualified QI. Your attorney, accountant, or real estate agent cannot be your QI. Even if the person seems trustworthy and competent, using a disqualified person disqualifies the exchange under the IRS's safe harbor rules.

Ignoring mortgage boot. Investors who focus entirely on rolling all their cash equity over sometimes forget that reducing the mortgage on the replacement property generates taxable boot. Model your transaction carefully with your CPA to confirm all three variables — value, debt, and equity — are handled correctly.

Entity mismatch. If the property is held in an LLC, the LLC must do the exchange. An individual member cannot exchange their interest in the LLC's property as if it were their own property. Get your entity structure reviewed before you list the relinquished property.

Assuming the replacement property doesn't have to be "held for investment." The replacement property must be acquired with the intent to hold it for investment or business use. Acquiring a replacement property that you immediately convert to your primary residence, sell, or flip will likely cause the IRS to disallow the exchange. The general guidance is to hold replacement property at minimum two years — and to have documented evidence of investment intent before any use changes.

Missing the tax extension deadline. If your exchange period spans two calendar years, filing a tax extension for the year of the sale is essential to preserve the full 180-day exchange window. Without an extension, your tax return due date becomes the effective deadline, which could be April 15 — potentially cutting your exchange period significantly short.

A Note on Political Risk: Is Section 1031 Going Away?

The 1031 exchange has been the subject of proposed reforms in every significant tax debate of the past decade, and DFW investors understandably want to know whether the provision is safe.

As of mid-2026, Section 1031 has not been limited or repealed under any enacted legislation. The TCJA of 2017 did eliminate 1031 treatment for personal property while preserving it for real estate — that limitation is already law. Proposals to cap the deferral at $500,000 per year or to eliminate the provision for high-income investors have been floated repeatedly but have not passed.

The political durability of Section 1031 comes from the breadth of its beneficiaries — not just wealthy investors, but farmers, small commercial property owners, family businesses, and estate holders across the income spectrum. Significant real estate industry lobbying also consistently defends the provision. That doesn't guarantee its future, but the provision has survived every recent tax overhaul.

Plan exchanges under current law. If the law changes, adjust. Do not avoid completing a beneficial exchange today on the speculation that the tax code might change in a favorable direction.

The North Texas Investor's Takeaway

If you own investment real estate in DFW — a rental home in McKinney, a small commercial strip in Plano, a warehouse in Garland, raw land in Celina — and you're thinking about selling, a 1031 exchange should be the first tax conversation you have, not an afterthought.

The DFW market has produced substantial appreciation across property types over the past decade. Texas's lack of state income tax means the federal tax you'd pay on a sale is the only tax you'd defer — a significant starting advantage over investors in most other states. And with DFW continuing to attract population growth, job creation, and new development, the inventory of viable replacement properties within the market — and the cross-market opportunities to exchange into other growing metros — is substantial.

What you need before any exchange:

A CPA with 1031 experience who understands the basis calculations, depreciation recapture implications, and the long-term basis impact of successive exchanges. General practice CPAs sometimes lack the depth of experience to optimize multi-exchange strategies.

A qualified intermediary engaged before you close on the relinquished property — not after. Research them carefully, verify their bonding and insurance, and confirm they use segregated accounts.

A real estate attorney for any transaction involving entity structure questions, partnership interests, tenancy in common interests, or reverse and improvement exchange structures.

A knowledgeable buyer's agent on the replacement property side who understands the 45-day and 180-day deadlines and can help you identify and contract on replacement properties within the exchange timeline.

OnDemand Realty works with North Texas investors navigating 1031 exchanges regularly — both on the sale side and the acquisition side. If you're evaluating a sale of investment property and want to understand how the exchange timeline works in the current DFW market, reach out.

Categories

Recent Posts